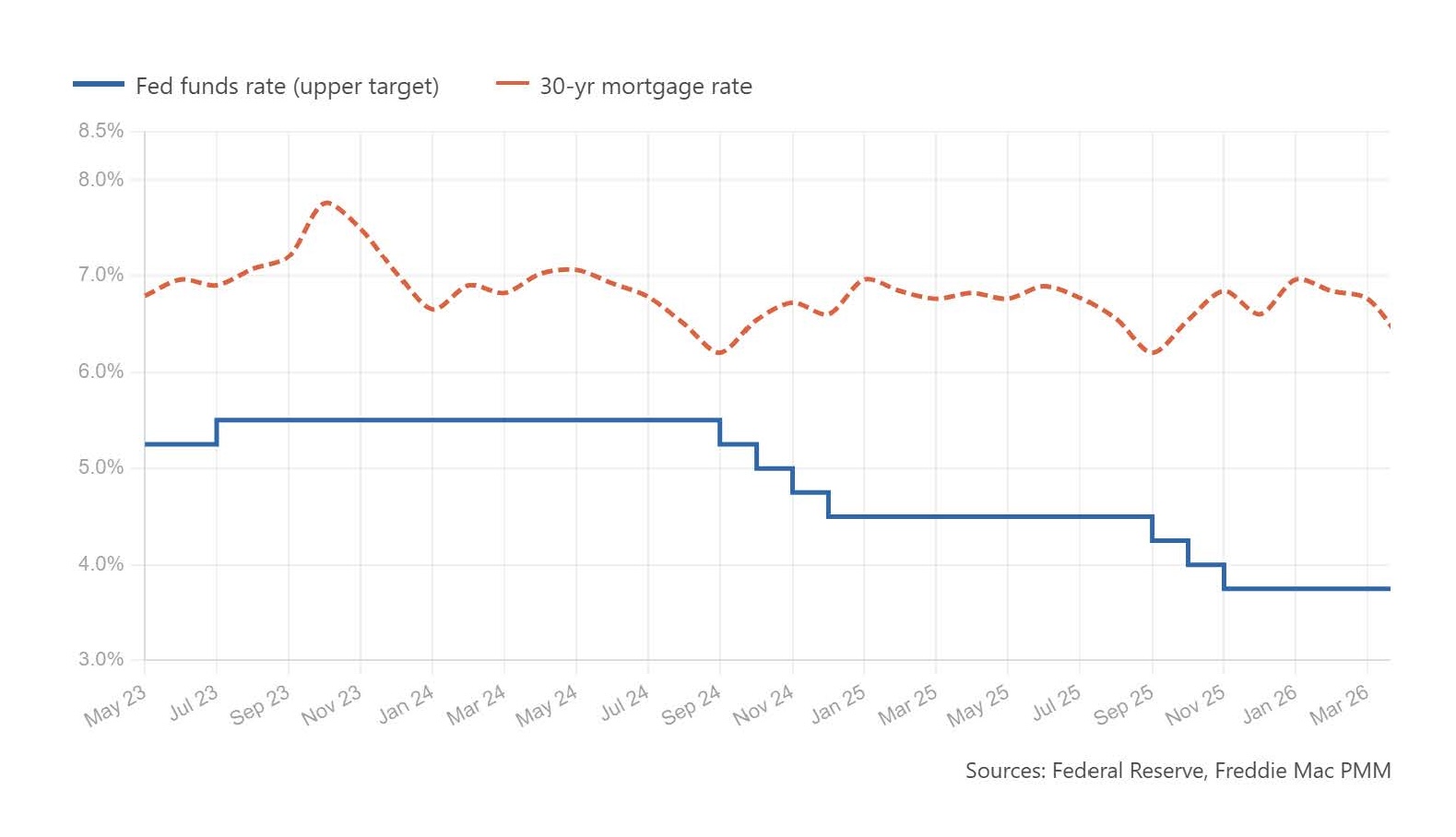

We frequently hear comments to the extent, “as soon as we get rid of Jay Powell, mortgage rates will go down!”

Whether you like or hate Jay Powell, the Chair of the Federal Reserve Board doesn’t set mortgage rates, and doesn’t even make the final decision about setting the short-term Fed Funds rate. To answer that question, the Federal Reserve’s monetary decisions really don’t impact mortgage rates, at least not directly.

The Federal Open Market Committee is composed of 12 voting members whose job, among other things, is to vote on and set the target range for the federal funds rate. While the Chairman has a vote, they cannot veto the Committee's decision or set rates on their own. Kevin Warsh will likely be the next Chairman beginning May 15, 2026, but even if he votes in June to lower rates, there’s no guarantee the fed funds rate or mortgage rates will go down.

What is the fed funds rate? It’s the target interest rate at which commercial banks borrow and lend overnight reserves to each other. It’s a short-term rate that banks use to set interest rates on short-term loans, such as credit cards and personal loans.

Mortgage rates, however, are typically longer-term loans, and those rates are reflected in the yield for 10-year Treasury notes. Treasury yields are determined by a host of factors, including inflation. That means, just because the Federal Reserve raises or lowers short-term borrowing rates doesn’t mean mortgage rates will increase or decrease.

In fact, mortgage rates sometimes move in the opposite direction from the fed funds rate. This is because lower short-term rates juice the economy by allowing businesses and consumers to buy more, which could lead to higher inflation. Bond investors hate inflation.