Averages Mean Nothing In Retirement

Return sequence, or return sequencing, is a phrase used to describe the year-over-year investment returns experienced by a portfolio for a select period. This sequence could look something like this over a 5 year period:

Year 1 Return: 5.00%

Year 2 Return: -2.00%

Year 3 Return: -10.00%

Year 4 Return: 7.00%

Year 5 Return: 15.00%

Average = 3% Yearly

If you have $100,000 invested during this example 5 year period this is what your portfolio would have looked like:

Starting Amount $100,000

After Year 1: $105,000

After Year 2: $102,900

After Year 3: $92,610

After Year 4: $99,092.70

After Year 5: $113,956.60

Average = 3% Yearly

That is an example of a Return Sequence.

Fixed Interest Instead of Average

What if you received a fixed rate of interest at 3% each year, would your account be the same value?

Lets check it out!

Starting Amount $100,000

Year 1 Return/Amount: 3.00% / $103,000

Year 2 Return/Amount: 3.00% / $106,090

Year 3 Return/Amount: 3.00% / $109,272.7

Year 4 Return/Amount: 3.00% / 112,550.88

Year 5 Return/Amount: 3.00% / $115,927.41

Wait, why is it more if it is the exact same average of 3% in both examples?

Lets look back at the graph above!

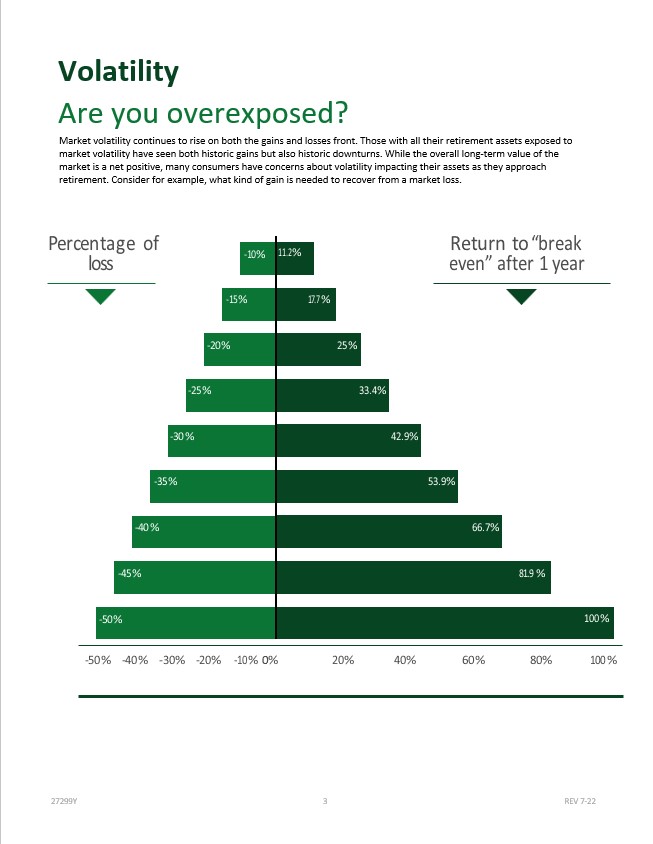

When you have a loss in a portfolio from market volatility or a withdrawal that made the account decrease you now find yourself in a hole that you have to climb out of. That requires a larger gain needed to return back to break even from the prior year.

The graph above shows how much of a return you would need to break even after a loss.

A 50% loss would need a 100% gain to break even. Is that possible?

Short answer - NO!

A Fixed & Indexed Annuity eliminates this risk due to your account always have a floor of 0%, meaning you can never experience a loss.

The more you know.